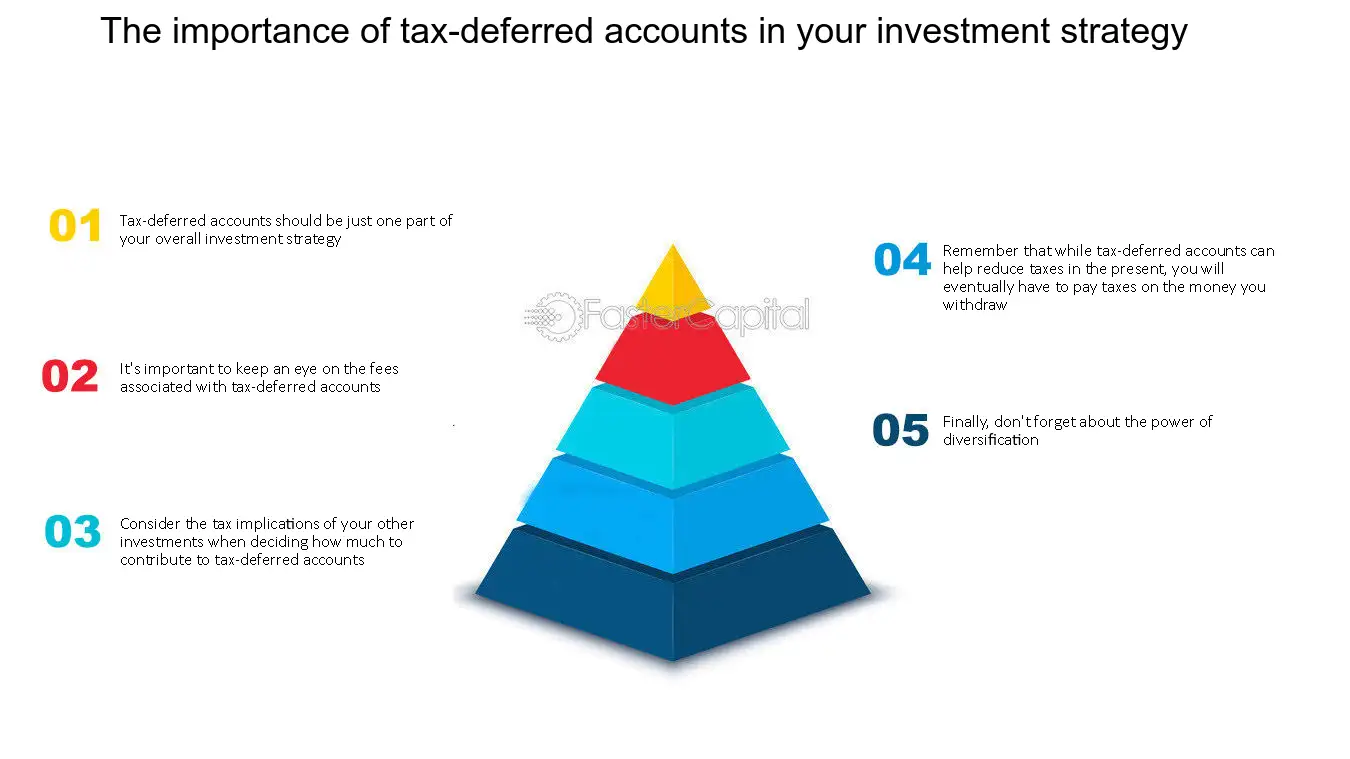

Strategic Use of Tax-Deferred Accounts in a Comprehensive Investment Plan

Tax-deferred accounts can be a strategic component of a diverse investment portfolio, helping investors grow wealth while managing taxes. Integrating these accounts wisely can provide tax advantages and complement other account types, making them valuable for a balanced financial plan. Looking to build a balanced investment plan? finance-phantom.org connects investors with educational professionals who can help integrate tax-deferred accounts into your broader strategy.

Tips for Integrating Tax-Deferred Accounts into a Diversified Investment Portfolio

A well-rounded portfolio mixes different types of investments, and tax-deferred accounts can play a valuable role in that mix. By deferring taxes on growth and income, these accounts can provide an advantage over time. The key to making them work effectively, though, is balancing them with taxable and tax-free options.

Consider diversifying between tax-deferred accounts, like 401(k)s or Traditional IRAs, and Roth IRAs (tax-free) or regular brokerage accounts (taxable). Each type has a distinct purpose.

Tax-deferred accounts are ideal for long-term growth, while taxable accounts are more flexible for accessing funds earlier. For example, taxable accounts allow for gains to be taxed at lower capital gains rates, while Roth IRAs grow tax-free. It’s like having a mix of tools in a toolbox, each ready for a different purpose.

Some people also like to keep higher-growth assets, like stocks, in tax-deferred accounts so that they don’t pay yearly taxes on those gains. On the other hand, bonds and dividend stocks might work well in taxable accounts, where lower tax rates can apply.

This combination lets tax-deferred accounts handle growth, while other accounts provide liquidity and possibly lower taxes for income-producing assets.

One piece of advice? Use asset location strategies to take advantage of tax treatment differences between account types. Over time, this method can boost returns and reduce the tax burden, which helps preserve your savings.

Managing Risk and Planning for Tax-Efficient Withdrawals

Balancing risk is critical in any investment plan, and tax-deferred accounts are no exception. Since these accounts often form a major part of retirement savings, it’s wise to review risk regularly.

For example, consider shifting to more stable assets, like bonds, as retirement nears. This helps protect the account’s value against market downturns just before you need to start withdrawals.

Planning withdrawals from tax-deferred accounts takes strategy, too. Since all distributions count as regular income, large withdrawals could bump up the tax bracket in retirement.

A good approach is to spread withdrawals over several years. Picture it like pacing yourself at a buffet—you don’t want to load up all at once. Gradual withdrawals can help keep tax rates manageable while providing needed income.

For added tax efficiency, some people start taking distributions early in retirement, before Required Minimum Distributions (RMDs) start at age 73. This method can reduce the account balance over time, leading to smaller RMDs and lower taxes down the road.

Another tip is to coordinate these withdrawals with other income sources to control overall taxable income. By managing both risk and timing, it’s possible to make the most of every dollar saved.

Importance of Consulting with a Tax or Financial Advisor to Optimize Tax Benefits and Account Choices

Consulting a financial or tax advisor is often the best way to get a clear picture of how tax-deferred accounts fit into the overall plan. Advisors bring expertise in tax law, financial planning, and retirement accounts, which helps in navigating complex rules and making effective choices.

For example, an advisor can help in selecting the right types of accounts to match specific goals, like growth, income, or legacy planning.

They can suggest ways to blend Roth accounts with tax-deferred savings, creating flexibility for tax-efficient withdrawals. Advisors also stay up to date on changes in tax law, such as the Secure Act’s adjustments to RMD ages, which can impact long-term strategies.

An advisor’s guidance is also helpful for families planning to pass on assets to heirs. Tax-deferred accounts are usually subject to taxes at the time of inheritance, but with a solid plan, it’s possible to reduce the impact. Think of it like having a GPS for your financial journey—an advisor can guide you through unknown terrain.

In addition, advisors offer insights on adjusting investments as retirement nears, from managing RMDs to planning distributions in ways that keep the tax burden low. Working with a trusted professional is a wise step for anyone serious about protecting and growing their retirement savings.

Conclusion

Incorporating tax-deferred accounts into an investment plan offers both tax savings and long-term growth potential. With the right strategy, these accounts can serve as the foundation of a tax-efficient portfolio. Working with a financial advisor can further help align these accounts with your overall goals, optimizing both growth and tax outcomes for retirement.